Quant Journey & Career

To Do & To Learn List

https://www.youtube.com/watch?v=qvFYzJ8-zbQ

Computer Science

• Language:

Python, SQL, HTML, CSS, Javascript, Angular

• Machine Learning:

Random Forest, Neural Networks, Decision Tree, Clustering, Dimensionality Reduction, Ensemble

• Data Manipulation:

Numpy, SciPy, Pandas, Statsmodel

• Data Visualisation:

Matplotlib, Plotly and Cufflinks, Seaborn, PyPlot, Bokeh

Math

• Calculus and Linear Algebra

• Optimization (Taylor Series, Markov Processes)

• ODE and PDE

• Stochastic Calculus (Martingales, Brownian Motion, Stochastic Integrals, Stochastic Differential Equations, Ito’s Lemma, Feynman-Kac)

• Binomial Asset Pricing

Statistics

• Regression (OLS, GLM, Logistic, and etc.)

• Time-series (ARIMA, GARCH, ECM)

• Nonparametric Regression (Splines, Kernel, Locally Weighted Regression)

• Data Exploration (Density Estimation, Normality Tests, Monte Carlo, Copulas

- Data Cleaning and Reduction (Cluster Analysis and Stats Theory)

Finance

• Equity (Stock Analysis, Diversification, Technical Analysis, Finance Theory)

• Fixed Income (Rate Curves, Pricing, Duration, TVM)

• Derivatives (Black Scholes, BDT, Stochastic Volatility Model, Volatility Smiles and Theory)

• Portfolio Optimization (CVaR, Efficient Frontier)

• Arbitrage Theory and Statistical Arbitrage

• Risk Management (VaR, Statistics, Credit Risk, Market Risk, Liquidity)

Inital List

1.0) Tech Skills

-Python, C++, C#, R, Matlab -> Programming

-Numpy, SciPy, Pandas, quantdsl, statistics -> Data Manipulation

-Statsmodel -> Explore data, estimate statistical models, and perform statistical tests.

-pyfin, vollib, QuantPy, ffn, pynance, tia -> Financial Instruments

-Tensorflow & ML, Keras, Scikit-Learn, Pytorch -> Machine Learning

-ZipLine, QTPyLib, PyAlgoTrade, Pybacktest, bt, backtrader, finmarketpy -> Backtesting

-Ultrafinance, TWP -> Data Collection

-IBridgePy, IbPy -> Interactive Broker Trading

-Blueshift, Quantiacs, Quantopian -> Open Source Python Trading Platforms

-Linux environment & shell scripting

-Pandas-datareader -> FInancial data from Google, World Bank

-TA-Lib -> Technical analysis of financial market data.

-PyMC3 ->Write down models using an intuitive syntax to describe a data generating process.

-MlFinLab -> Turning academic research into practical, easy-to-use libraries

-NLP -> NLTK. TextBlob, spaCy

2.0) Financial Analysis

2.1) Quantitative portfolio management techniques:

2.2) Mathematical models and methods

2.3) Statistical

2.4) Econometric models

2.5) Quantitative-modeling

2.6) Risk-modelling (Model development/validation)

3.0) Trading Strategy

Momentum strategy (Divergence or trend trading)

Reversion strategy.

Forecasting strategy

High-Frequency Trading (HFT) strategy

Stock Market Strategies — Seasonal Anomalies

3.1) Result Analysis

-Calmar Ratio

-Sharpe Ratio

-Drawdown

-Compound Annual Growth Rate (CAGR)

-Distribution of returns,

-Trade-level metrics

3.2) Backtest

Tools: Pandas, zipline and Quantopian.

Pitfalls:

-External events, such as market regime shifts, which are regulatory changes or macroeconomic events

-Liquidity constraints, such as the ban of short sales

-Yourself:

-Overfit a model (optimization bias)

-Ignore strategy rules because you think it’s better like that (interference)

-Introduce information into past data (lookahead bias).

Backtesting Components (Four essential components)

-A data handler, which is an interface to a set of data

-A strategy, which generates a signal to go long or go short based on the data,

-A portfolio, which generates orders and manages Profit & Loss (also known as “PnL”),

-An execution handler, which sends the order to the broker and receives the “fills” or signals that the stock has been bought or sold.

3.3) Optimisation

Improve the model on a continuous basis

-KMeans

-k-Nearest Neighbors (KNN)

-Classification or Regression Trees

-Genetic Algorithm.

-Reinforcement learning, stochastic optimization, Bayesian frameworks, deep learning & machine learning

Working with multi-symbol portfolios

-Just incorporating one company or symbol into your strategy often doesn’t really say much.

-You’ll also see this coming back in the evaluation of your moving average crossover strategy.

Risk management framework

Event-driven backtesting to help mitigate the lookahead bias

4.0) Portfolio Maker

-Deploy Jupyter online

-Automated Trading System -> FXCM, Oanda, Quantopian, Quantconnect

-Running Your Algorithms in Cloud -> AWS EC2 Instance

-Forex Algorithmic Trading -> C++ , MQL4

-Trading Type: Forex, Cyrto, Equity

-Test: MQL4, Quotopian, Quantconnect, Freqtrade

-Algo Platform List

Quantopian (Python)

Backtrader (Python)

Quantconnect (C#, F#)

Quantrocket (Python), $$

-Data provider

Intrinio

Quandl

Norgate Data

-Execution Broker-Dealers

Interactive broker

Alpaca

5.0) Programming competitions

- Kaggle, CrowdAnalytix, CrowdAI, DrivenData

Quantiacs

https://www.quantiacs.com/For-Quants/Quant-Tutorials/Videos.aspx

Quantconnect

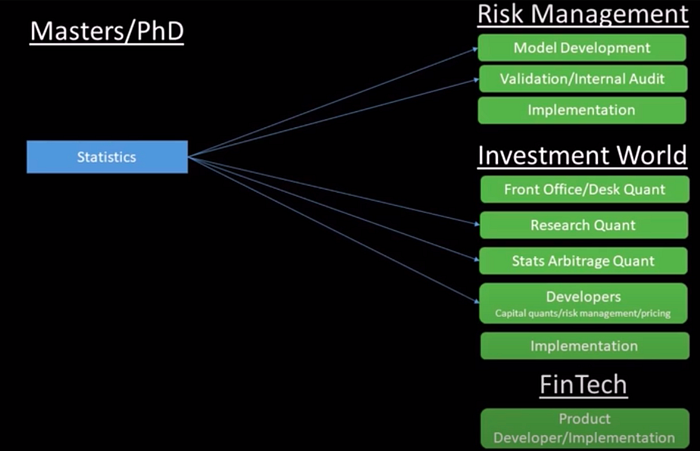

Career Path

https://www.youtube.com/watch?v=ptd4XicBUnY

1) Front office/desk quant

2) Model validating quant

3) Research quant

4) Quant developer

5) Statistical arbitrage quant

6) Capital quant

https://www.youtube.com/watch?v=Ubg0fX2mLUQ

https://drive.google.com/file/d/1ENm1RH9rwrnCuSq8cc9awuwekaETEDIA/view